I will assume readers are familiar with Yelp’s basic business. If not, I recommend reading the “Company Overview” section of the 10K.

YELP isn’t a natural fit for either growth-oriented investors or value-oriented investors, and I think that makes it an interesting stock. Growth investors won’t love the dated, internet 1.0 brand and the lack of user growth. Value investors won’t love the lack of GAAP profitability and heavy usage of share-based compensation. Neither camp will like the competitive threat from giant rivals like Google. For those willing to dig beneath the surface, however, I believe YELP offers a compelling opportunity.

Let’s start with a review of the financials, beginning with the top and bottom lines:

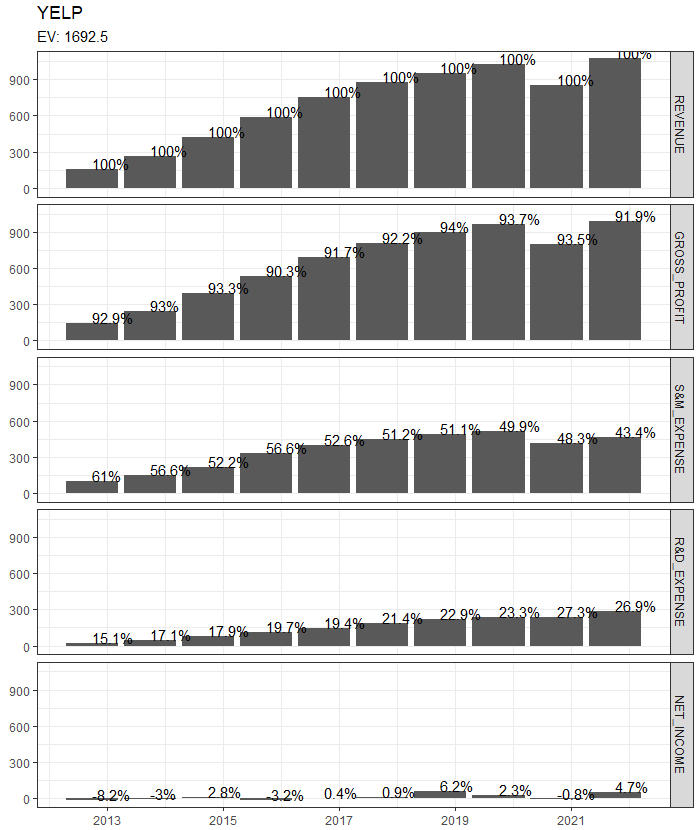

Excepting the pandemic-impacted period, revenue has been in a consistent uptrend for a decade, though the pace has begun to level out recently. Earnings, on the other hand, show a completely different contour. They hover near zero, exhibit no uptrend, and are small relative to enterprise value (last 12mo P/E is in the high 40s at the current price of $30.45). What is going on? Lets take a look in the middle:

Gross profit has kept pace with revenue - gross margins have fluctuated in the low-mid 90s range. Operating income, however, is managed to zero (Amazon style), with increases in gross profit funding ever larger marketing and R&D budgets. The key question for valuation purposes is to identify the amount of R&D and marketing spend that is necessary to simply keep the company running at its current pace (maintenance R&D/S&M) vs the amount that represents investment in the future and which therefore should be classified as reinvested earnings.

Lets take a look at S&M first. Yelp’s S&M profile has changed over the last three years. Prior to the company’s strategic pivot in 2018, S&M spend was largely on “local” salesforce, meaning salespeople who would build connections with local businesses and attempt to sell them on “term”, i.e. 12mo+, advertising arrangements. In 2018, the company realized this wasn’t a scalable solution and pivoted to non-term contracts (allowing businesses to try advertising out without committing to a year) primarily via the self-service channel. Building out the self-service channel and the accompanying attribution, etc. has been one of the major uses of R&D dollars. When the pandemic hit, the company slashed its local salesforce dramatically in accordance with its strategic pivot to focus on multi-location and self-serve. I don’t believe Yelp ever intends to ramp the local sales force back, and we can see the benefit in the lower S&M margins LTM (43% vs low 50s pre-pandemic). What remains of the salesforce is focused on “multi-location” advertisers, who are more sophisticated and have bigger budgets, and who therefore allow for improved S&M leverage.

For a business that is growing like Yelp, I typically will classify a portion of S&M spend as investment rather than as an expense. The positive impact of marketing is almost always longer-tailed than a year. For example, if Yelp’s salesforce spends time creating a relationship with a major chain of coffee shops, in the future, assuming the value proposition isn’t diminished, the marketing team will be able to maintain the relationship with much lower investment and can instead focus on pursuing new prospects. Some of the salesforce time spent each year therefore provides a benefit in future years, and is more like investment than maintenance spend. I typically classify ~30% of S&M spend as investment and the rest as an expense. The idea is that Yelp could cut S&M by 30% and still manage to keep PALs (Paying Advertising Locations) stable, so we should consider it earnings power. Thirty percent of LTM S&M budget is ~$140M.

Now lets consider R&D. While S&M spend as a percent of revenue has declined of late as the company scales, R&D spend as a percent of revenue has ramped as the company adds a slew of new products and features. The most important use of R&D spend has been on ad-tech, which allows for better-targeted ads and magnifies value per impression. The company has also used R&D budget on building out the “self-service” tech stack, mentioned above, which has allowed the company to leverage S&M expense. Other products include:

Request a Quote - A standardized format for requesting estimates from service providers (think movers, landscapers, plumbers, etc.). Yelp users who fill these forms out have a very high purchase intent and Yelp sells these leads to service businesses. Last year, while only ~10% of Yelp page views and searches were service business related (90% fell in the restaurant/retail/other category), service-related ad products like request-a-quote generated just over 60% of revenue. This product is similar to ANGI’s primary product.

Yelp Audiences - Similar to FB audiences. People who browse Yelp looking at plumber listings are very likely to hire a plumber in the near future. Yelp buys ad space on other sites, like the Washington Post for example, and resells it at a markup to plumbing businesses wanting to target a high-intent customer. This product opens the door for other types of advertisers as well. For example, Budweiser may want to show beer ads to people who have visited bars recently, etc.

Yelp Guest Manager - Reservation/waitlist software offering. Yelp users can make reservations directly from the app.

Eventually the low-hanging R&D fruit will have all been picked, but management claims that point is a ways off. A recent focus is on the Android side. From the quarterly results:

”Bringing the user experience on our Android app to parity with the iOS experience presents an opportunity to drive greater levels of user engagement and monetization. In the first quarter, our teams significantly improved the map view search experience on our Android app and executed several back-end improvements, resulting in a 20% increase in Android ad clicks following their implementation in March 2022.”

In cases like Yelp, where management deliberately keeps operating income at zero while plowing cashflow into R&D, I believe it is a mistake to classify the whole line item as an expense. Some portion of this spend represents earnings power that is reinvested into the business. As with S&M, the key is to identify the portion of R&D spend that would be required merely to tread water versus the portion that drives growth in the future. What portion of R&D spend could be turned off without causing a drop in gross profit? Five years ago, Yelp spent $187M on R&D. Eight years ago they spent $75M. At both those points in the past the company kept growing despite the lower spend. In the last year Yelp spent $289M on R&D. It’s hard to say for sure, but I’d guess only around $100M of that spend is truly maintenance. That means ~$189M represents earnings reinvested.

The sell-side by and large seems to think about Yelp valuation using multiples to adjusted EBITDA, a measure which adds back share-base compensation. Given that share-based compensation represents virtually 100% of the FCF of the company, this always seemed odd to me; Yelp can grow this measure simply by increasing the stock proportion of employee compensation. It gets even odder when we consider that Yelp then repurchases roughly the same amount of shares as it issues in SBC. Why stock-based compensation should be included in a profitability measure when the company simply takes the cash it saves via SBC and buys back the shares it issued is beyond me. I think it is better, if more arbitrary, to attempt to tease out the portions of S&M and R&D spends that should be considered earnings-reinvested when thinking about valuation. Yelp generated $43M of operating income over the last 12mo. I estimated in previous sections that ~$140M of their S&M budget and ~$189M of their R&D budget should really be considered earnings until the evidence shows Yelp is no longer getting a reasonable return on their excess spend. If we sum operating income and excess S&M/R&D, we get $372M, implying a ~4.5x EV/EBIT multiple.

Is a 4.5x multiple cheap? The answer depends on two things. First, are we sure Yelp is getting a good return on the investments it is making. If the return is close to or higher than the company’s WACC, a 4.5x multiple would be a steal. Second, will Yelp be able to withstand competitive pressure for consumer attention in the ratings/reviews landscape.

One exercise I like to perform when considering the first question is to examine historical return on investment spend. Lets assume we always classify 30% of S&M and 70% of R&D as being non-maintenance. Lets define “adjusted EBIT” as operating income plus 30% of S&M spend and 70% of R&D spend. Five years ago, the company had adjusted EBIT of $280M compared to a LTM adjusted EBIT of $386M. The company has relatively minor capex/D&A, so lets define investment spend as being solely that 30% of S&M and 70% of R&D. In that case, in the four years proceeding the LTM, the company spent a cumulative $559M on S&M investment and a cumulative $615M on R&D investment. This sums to $1,174M in total investment spend, which resulted in adjusted EBIT growth of $106M. Applying a 25% tax rate to adjusted EBIT gives ~$80M in earnings growth or a 6.8% ROIC. This is a fairly low number and certainly below the company’s WACC, but we should remember the LTM contain some residual pandemic impact (restaurant/retail/other ad revenue was $90M lower in 2021 vs 2019). If we perform the same analysis on the five years through the end of 2019, we get an ROIC of 16.4%. (Obviously there are hundreds of ways you can tweak this basic framework for considering recent ROIC, and many potential issues with the way I framed things. I think it is still a useful way of thinking through the impact of investment spend.)

Now, to address the competitive pressure issue. The bear case on YELP has long been that the company will be unable to compete with megacap tech, particularly Google, which can use its position as the homepage of the internet to siphon small business related search traffic to its own review portal. Indeed, Yelp user growth summing across all platforms (not a safe way to count unique users and greatly exaggerates the total MAUs, but I think still has some use as a metric) had stalled out even pre-pandemic, and still hadn’t recovered to pre-pandemic levels in 2021, seeming to confirm these fears.

I think the competitive issue is a serious one and worth spending time thinking through. There are a few arguments in support of Yelp’s competitive position. First, I would make the case that Yelp reviews are somewhat differentiated. A 2020 study by an FTC economist found that Yelp had a much more symmetric distribution of reviews than other sites, likely due to the high level of scrutiny they place on reviews. Whereas only around 30% of Yelp business listings have between 4 and 5 stars, over 50% of Google business listings do. Yelp would argue a balanced rating distribution allows for better consumer differentiation and builds user trust. At the current valuation, I would argue that even if only a fraction of consumers use Yelp, and only as a second opinion to Google, that would still be a win for traffic.

Second, I would argue that the shift to a mobile-app-based internet creates an opportunity for Yelp to sidestep the Google issue. The crux of the Google issue is that potential Yelp users must pass through a Google search result in order to reach Yelp content. On the way, they are offered a Google alternative that requires no clicks and occupies differentiated screen space. This gives Google the obvious edge in acquiring potential users searching via a desktop or mobile web browser, but this does not hold for users of the Yelp app, which is why transitioning users over to the app is a top priority for Yelp management. In theory, it is no harder to open the Yelp app and search for local business content than it is to open a web browser app and search for content, so if Yelp can acquire users who are accustomed to turning to the mobile app first it will be much harder for Google to poach those users.

Finally, and this argument holds the most weight for me, the best way to identify a moat is to observe a company face intense competition and walk away alive. The Google threat is not new, it has been ongoing for a decade. Certainly Yelp would have done infinitely better in a world where Google never ramped up competition, but the company managed not only to survive in the face of pressure but grew “adjusted EBIT” consistently through all of it. As the proportion of users accessing Yelp directly through their app increases (already iOS app users account for the majority of ad clicks) the competitive threat arguably weakens relative to what it has been in the past.

A few other notes I wanted to mention before wrapping up:

Yelp is run by one of its co-founders, Jeremy Stoppelman, a member of the “PayPal Mafia”.

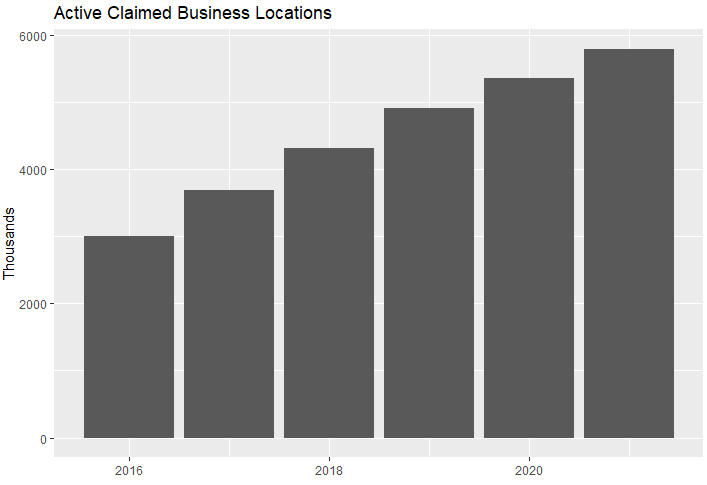

While Yelp user traffic fell during the pandemic, business owner traffic did not, and the pool of potential Yelp advertisers continues to grow as businesses focus more and more on their online presence. Here are active claimed business locations on Yelp:

The potential for Yelp to be acquired has been brought up in the bull case for many years now. An acquisition would not be surprising given the relatively bite-size EV and high strategic value.

While Yelp user traffic has stalled out, it would be much worse if user traffic had stalled out despite significant spend on user acquisition. The company mentioned spending only $11M over the past three years combined on user acquisition. The strategy seems to have been to first focus on expanding the value per user and honing the platform before making a push to acquire users. This sequencing makes sense and a push into user acquisition, made possible by the elevated lifetime value per user, could be an accretive next step.

How does Yelp’s R&D adjusted multiple compare to other heavy R&D company’s like FAAMG?

To wrap things up, I look at Yelp as a reasonably positioned business in a growing industry whose “real” multiple is kept artificially low because of its strategy of investing through the income statement. The obvious catalyst for outperformance would be for Yelp to prove its earning power by allowing future gross profit growth to flow through to net income instead of investing it in R&D and S&M. Over the last five years, Yelp has grown gross profit at an 8.3% CAGR. If next year Yelp grows gross profit by that amount, but lets the increase pass through to operating income instead of expanding investment, then operating income would grow from $43.1M to $148.6M and the EV-to-operating-income multiple would fall from 39.3x to 11.4x. There is not yet an indication Yelp intends to go this route, as the company believes there is still plenty of low hanging fruit for investment, but if the company is right about the investment potential then investors should be happy to wait for share price satisfaction. My thesis on Yelp really boils down to my belief that a large portion of the R&D and S&M spend is non-maintenance in nature, with my evidence for this being that the company still managed to grow despite much lower spend in the past, that the company clearly appears to be managing operating income to zero, and that the investment spend has seemed to have a satisfactory return historically.