Short $AAPL

Short $AAPL

AAPL has been over-earning and this will become apparent soon.

Summary: I will make the case that Apple, like the majority of companies, over-earned during late-2020 and 2021. This viewpoint does not appear to be priced in, and therefore I believe there is an opportunity to short AAPL, either outright or against another name.

The years 2020 and 2021 were economically extraordinary. What should have been a large negative economic shock turned out to be a tremendous boon thanks to unprecedent fiscal stimulus. In the US, the government paid more than the average wage in unemployment benefits, meaning few individuals suffered a drop in income. The US government also sent out thousands of dollars in checks to a large percentage of the population. Hundreds of millions refinanced their mortgages and achieved permanently lower payments. Many others took a break from mortgage payments altogether.

The net effect of all this was a huge surge in earnings for cyclical sectors. In some cases, like in specialty retail, the market clearly does not buy in to the surge in earnings (visible in compressed multiples), but in other cases, as with AAPL, the market assumes 2020/21 results reflect a new normal.

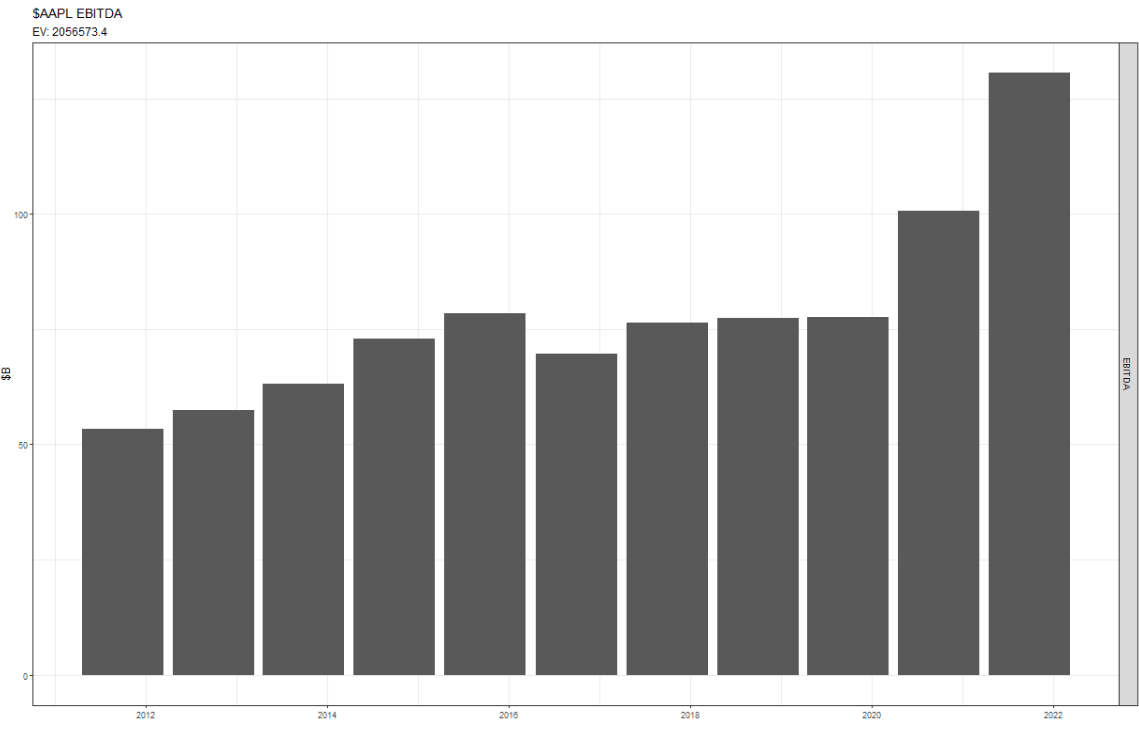

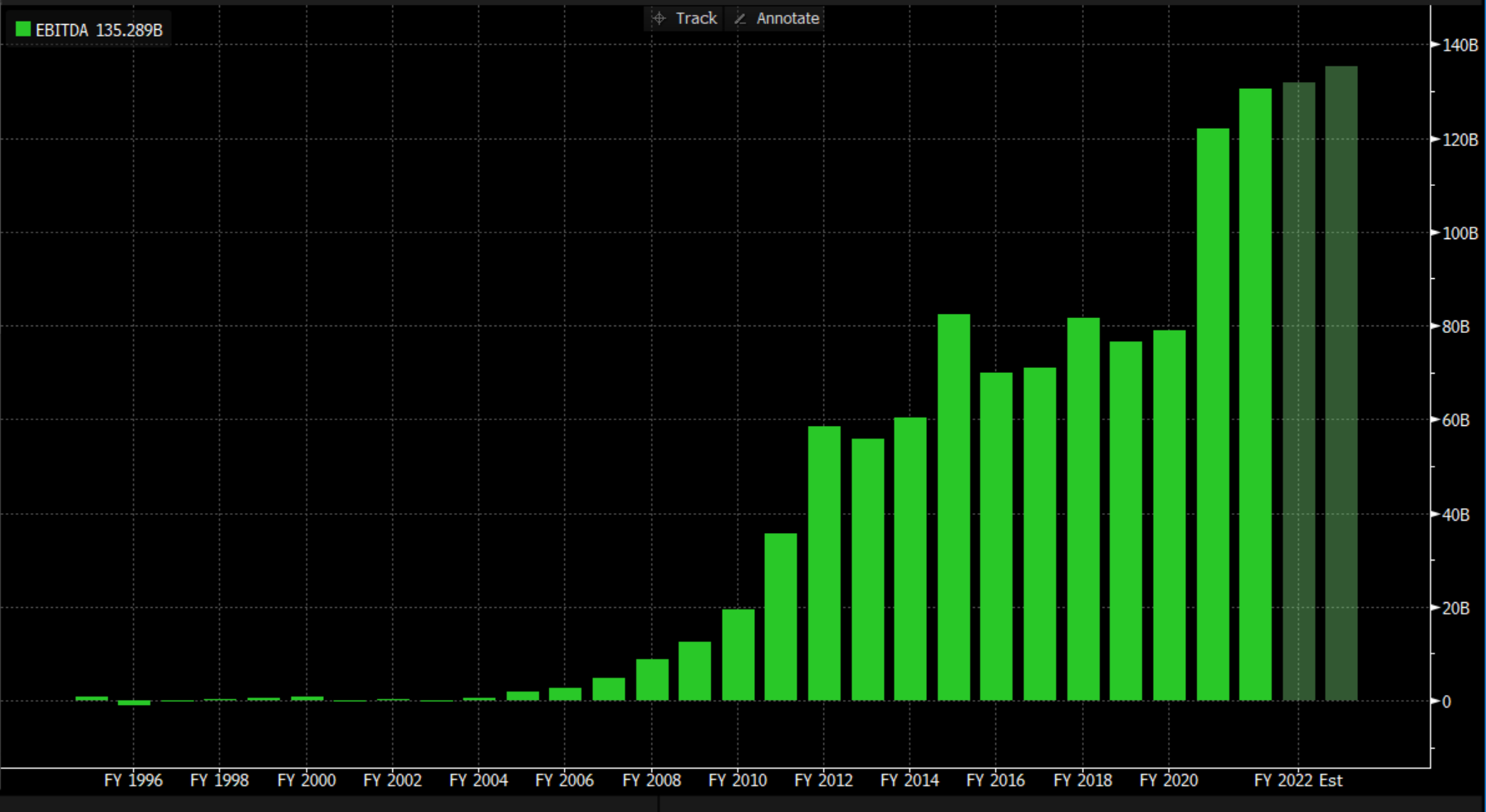

Let’s begin by taking a look at AAPL earnings. Here is EBITDA in the post-iPhone era (bars are discrete 12mo intervals):

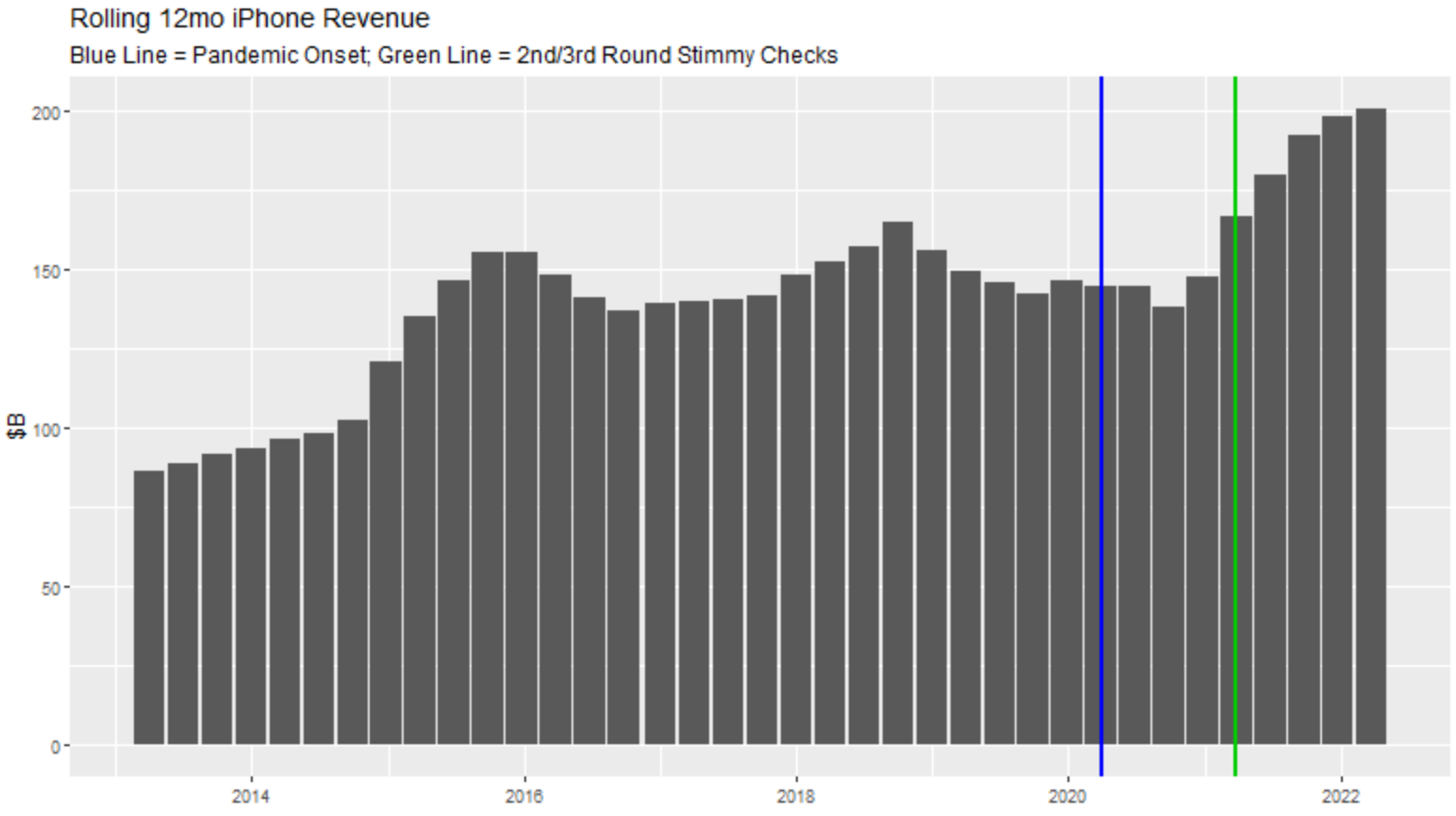

EBITDA steadily grew from 2011 to a peak in 2015, and flatlined from 2015-2019. Then, suddenly, an explosion of growth in late-2020 / early-2021! What new product or innovation was responsible for this? There weren’t any. There were, however, three rounds of stimulus checks and a temporary explosion in demand for WFH equipment. Lets take a deeper look at Apple’s reporting segments. First up is iPhone.

The blue line marks the start of the pandemic and the green line marks the first quarter impacted by the 2nd/3rd round of stimulus checks. So we see iPhone sales stagnant for ~6yrs, and then suddenly an explosion in sales on the heels of stimulus checks coincident with the dramatic rise in sales across many companies.

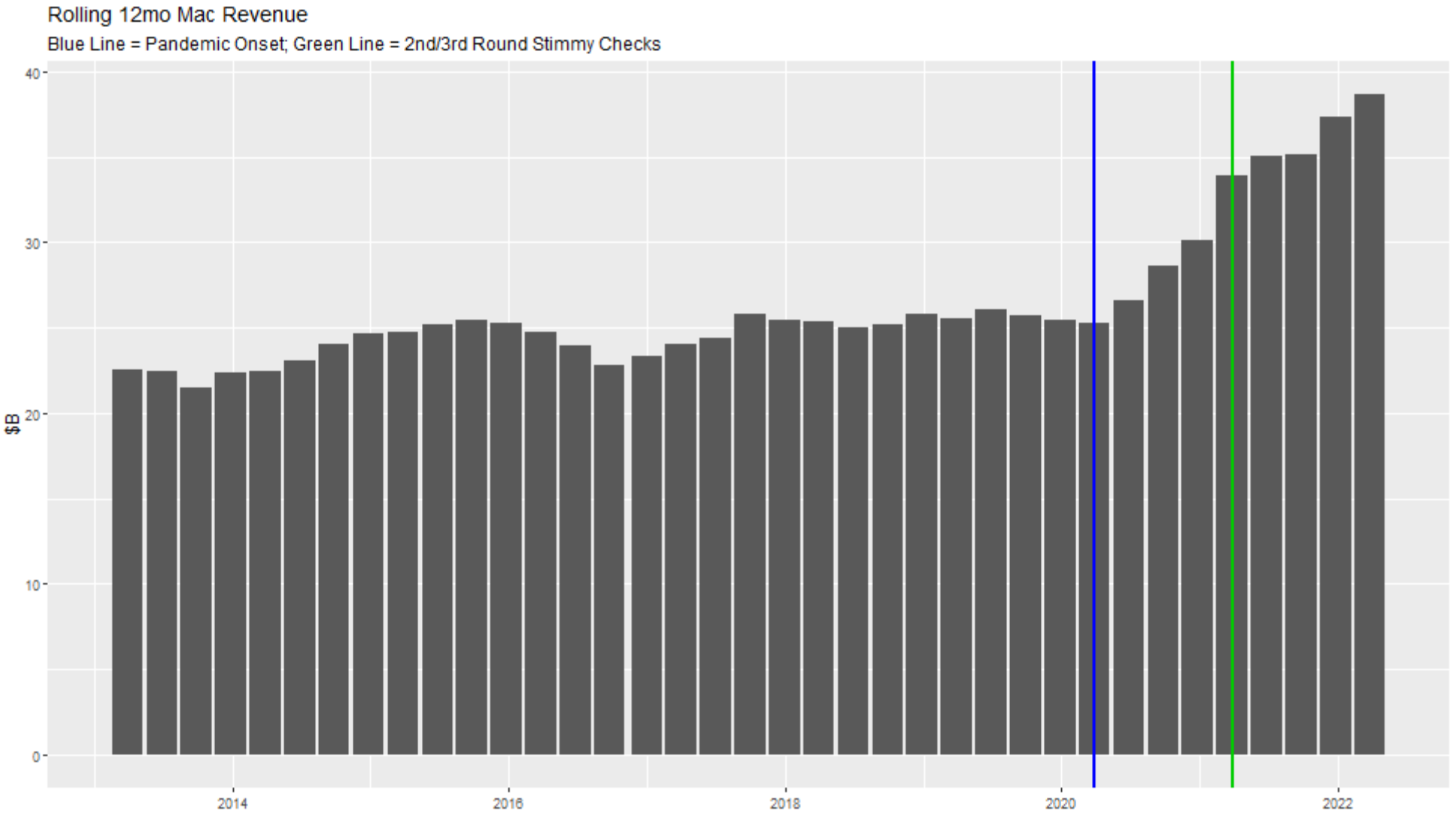

Next up is Mac:

As with iPhone we see stagnation in Mac revenues prior to the pandemic. Unlike iPhone, Mac sales begin to rise immediately after the onset of the pandemic (WFH boom) and then accelerate further following stimulus payments.

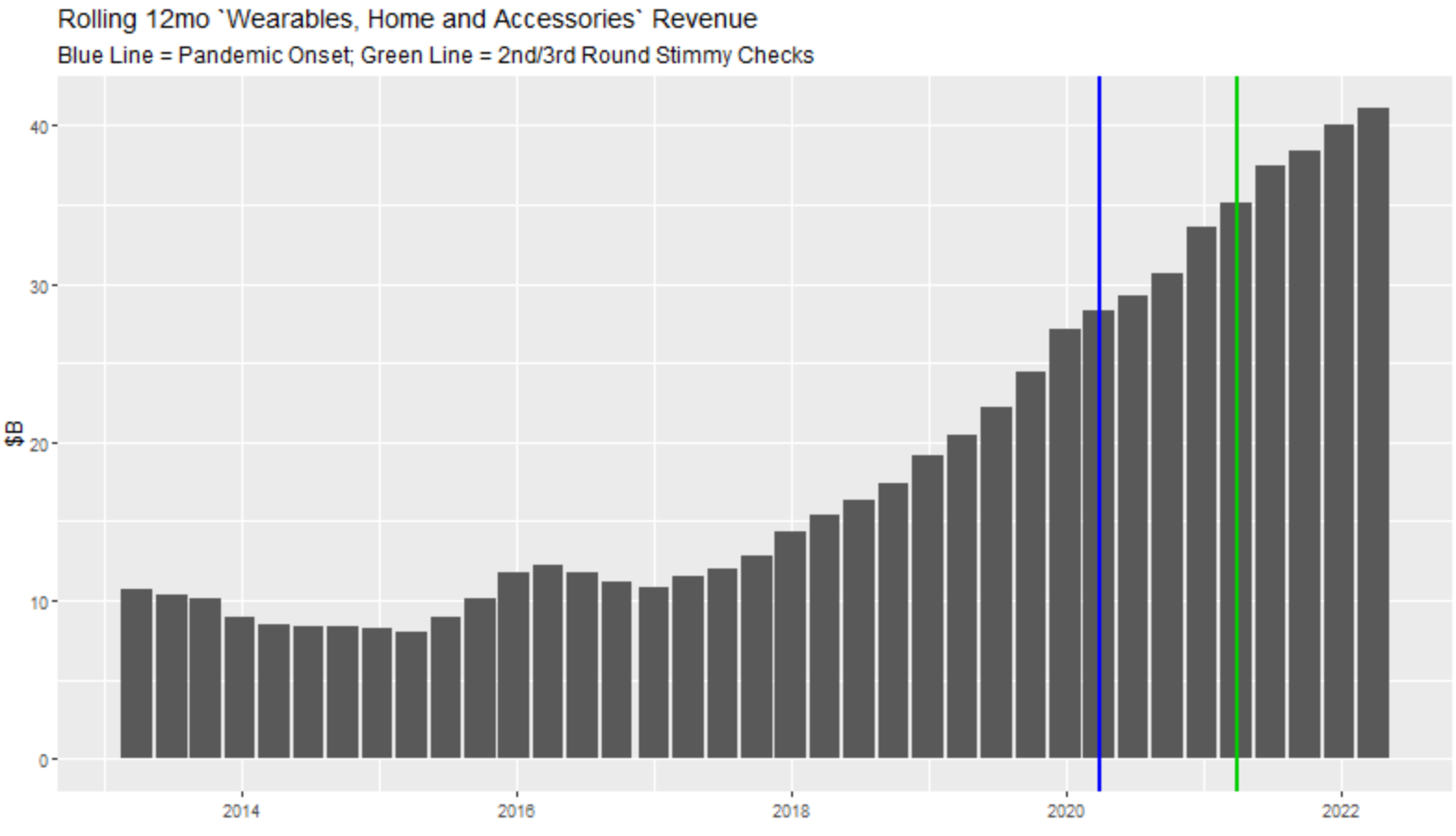

Now “Wearables, Home and Accessories”:

Here we see persistent pre-pandemic growth that continues smoothly through the pandemic period. This growth seems much more likely than iPhone/Mac growth to not only persist but continue growing.

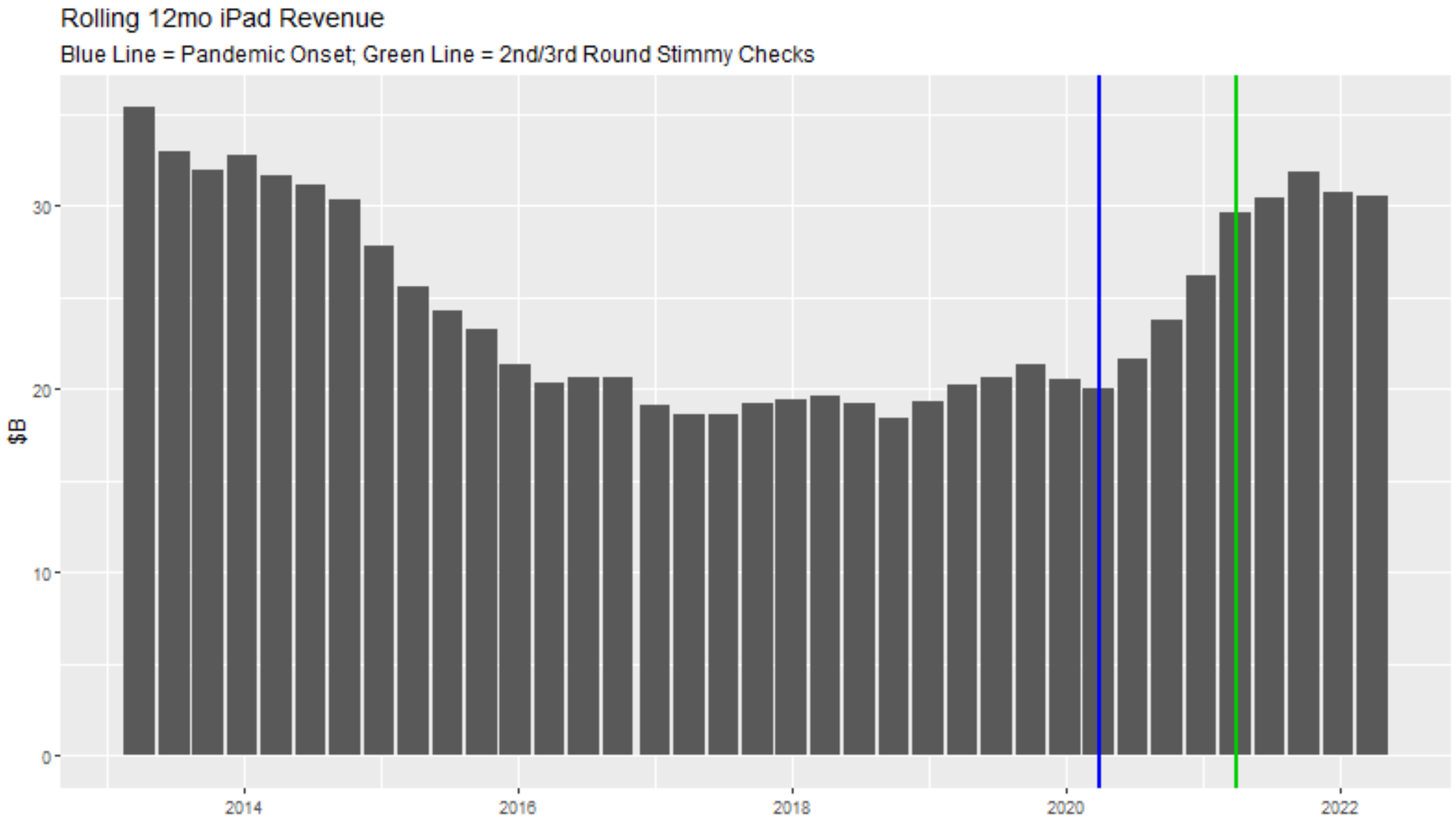

Now iPad:

iPad sales had been stagnant, then erupted in the pandemic era before beginning to level off more recently.

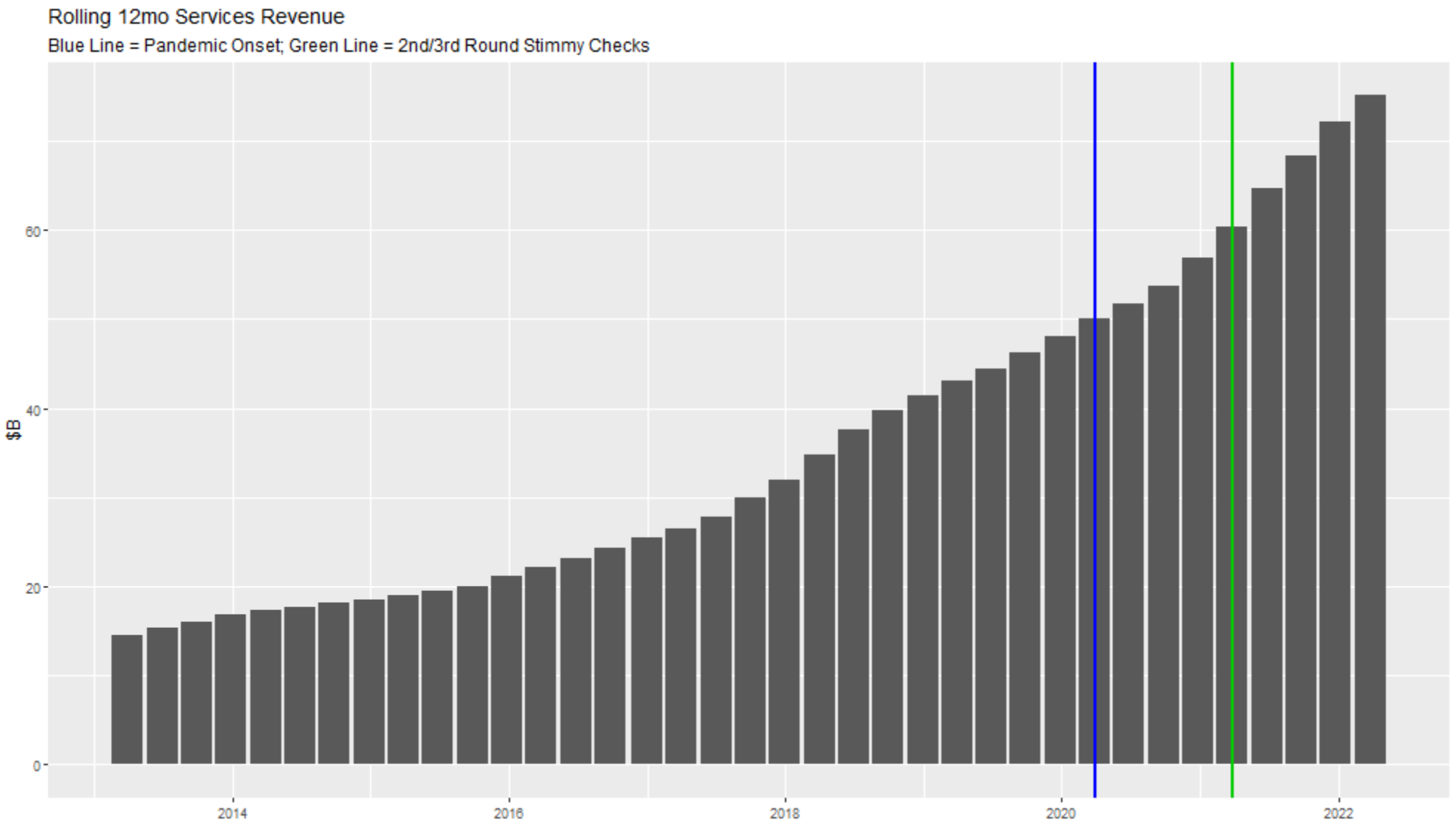

Finally, the services segment:

The “services” segment, like the “wearables” segment, enjoyed steady growth pre-pandemic which continued smoothly throughout the pandemic period. As with wearables, we might expect this trend to continue.

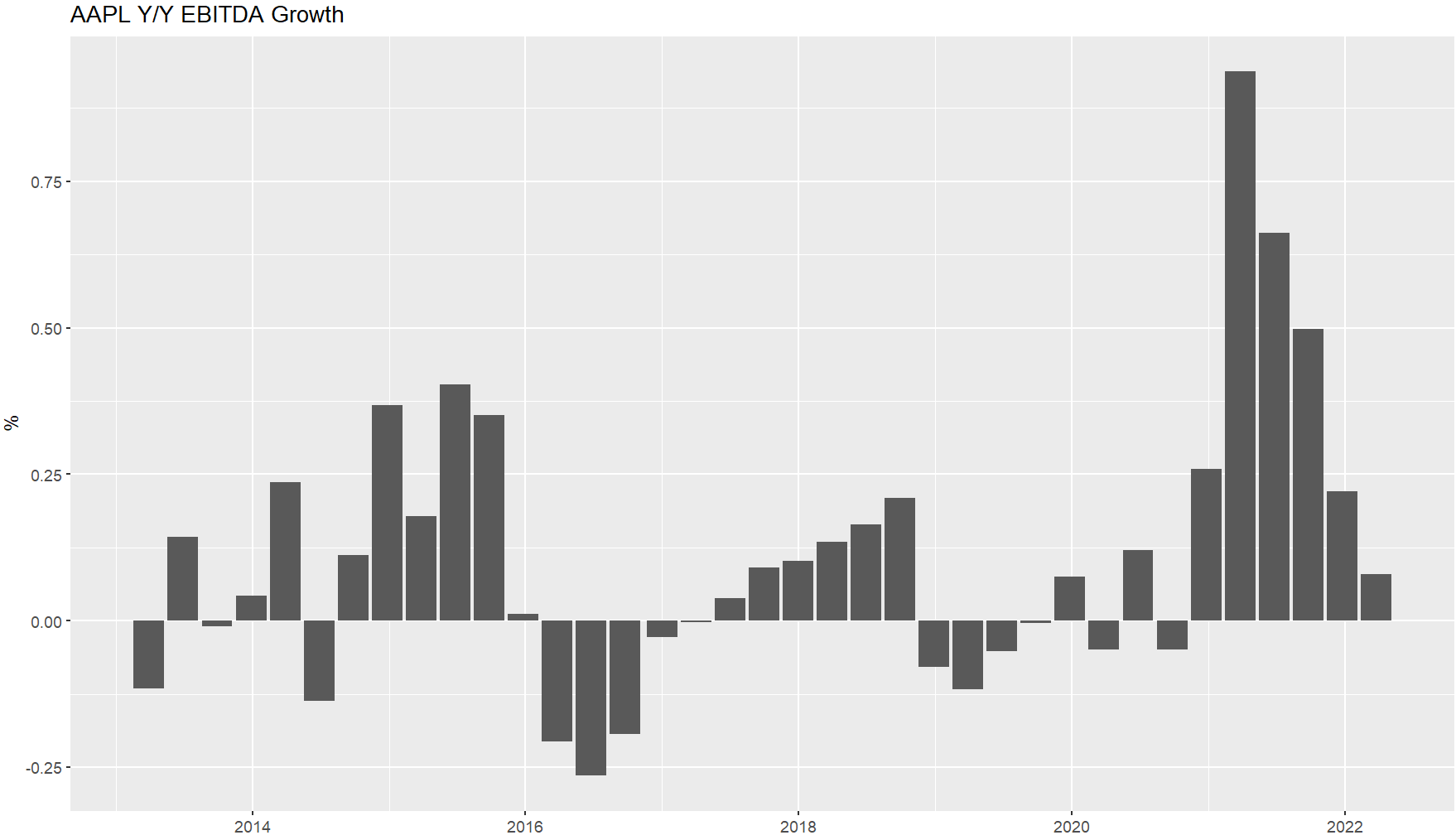

Summing things up, the iPhone, Mac and iPad segments were all experiencing stagnation prior to the pandemic, and then suddenly saw dramatic growth. Investors must decide, did the pandemic usher in a permanent uptick in the number of iPhones, iPads and Macs sold each year? Or is it more plausible that a temporary cocktail of unprecedented global stimulus and elevated need for WFM equipment and electronic entertainment drove the surge? I would argue the latter is much much more convincing, and I therefore think it is likely that the excellent operating performance we have seen from AAPL over the last ~24 months will fade driving declines in revenue and profitability in coming quarters. The second derivative of profitability has already turned and is approaching the psychologically important 0% level:

Making matters worse for AAPL, it can be argued that a portion of demand for their products over the last two years was pulled forward from future years. We might expect those who upgraded to a new MacBook for their WFH setup or who used a stimulus check to buy a new iPad to not need to upgrade again for a handful of years, which could weigh on near-term results. On top of this, economic tailwinds are turning into headwinds, creating the possibility that the 2023 operating environment might be worse than even the 2019 one.

How do we know this isn’t all priced in? After all, AAPL stock has had a large drawdown from peak. One way to evaluate what is priced in is to examine analyst expectations. Here is what I see on Bloomberg:

Analysts expect future results to exceed recent results over the next two years, which is inconsistent with my theory that AAPL over-earned in an exceptional and non-repeating operating environment.

Another way to think about pricing is to consider AAPL’s current EV/EBITDA multiple to 2019 results. In FY 2019 AAPL did 76.5B of EBITDA. Given a current EV of 2.19T, that puts EV-to-2019-EBITDA at ~29x. That could easily halve in the current valuation environment if EBITDA does indeed return to 2019 levels (I don’t anticipate a full return to 2019 levels given continued growth in the wearables and services segments, but it is possible).

A final way to demonstrate that the market has not priced in this scenario is to look at pre-pandemic EV. Apple EV at the end of 2019 was 1.18T, little more than half of the current EV.

To conclude, I think the evidence favors the idea that AAPL’s recent earnings results were fueled by an exceptional fiscal and cultural environment that is fast coming to an end. Making matters worse, the ~2023 economic backdrop seems set to be worse than even the 2019 backdrop, and some demand for AAPL products likely represents pull-forward which will weigh on near-term results. If this theory is true, we should expect AAPL earnings to decline substantially in coming quarters. The market does not seem to be pricing in this outcome. I am short $AAPL against stocks where I believe current pricing already embeds a decline in earnings to well below 2019 levels.

Edit: I wanted to add two counter-arguments I have received that I thought were reasonable. The first is that the pickup in iPhone sales might be wholly or in part due to the regulatory crackdown on Huawei. Huawei market sale losses happened around the time iPhone sales were surging meaning part of the expansion in iPhone sales is likely market share based and more sustainable. In my modeling I have assumed ~half. The second argument is on Apple M1 chips which were very well reviewed and may have played a role in the very strong Mac results. As with the Huawei argument, I think this is at least partially right. I believe this will be more than counteracted, however, by the unwind of pandemic demand pull-forward in coming year results.

Good thoughts, gonna share this in my bi-weekly curation newsletter this Sunday.